Everything You Need to Know about Mortgage Default Insurance

The toughest part of buying a home is saving up the down payment. With mortgage default insurance you can purchase a home for as little as 5% down payment…

The toughest part of buying a home is saving up the down payment. With mortgage default insurance you can purchase a home for as little as 5% down payment…

Add-backs and offsets are two different methods for accounting for the rental income from an investment property. If you are considering purchasing a rental property, understanding how add-backs and offsets work, is important when qualifying for your next mortgage. Please note that regardless of the method used, lenders do not use 100% of the rental…

What is BC Assessment? It’s January and people in BC have started receiving their property assessments. BC Assessment is a provincial Crown corporation that values all real estate property in British Columbia. Every year, BC Assessment sends property owners a Property Assessment Notice telling them the fair market value of their property as of July…

Large home purchases that require a mortgage present unique challenges in the Canadian Mortgage market. Sliding scales, director approval, multiple reviews, it all adds up to difficultly getting larger mortgages approved, unless you’re working with an experienced mortgage broker.

Since homes are expensive, a mortgage is a lending systems that allows you to pay a small portion of the home’s cost (called the down payment) upfront, while a bank/lender loans you the rest of the money. You arrange to pay back the money that you borrowed, plus interest, over a set period of time (knows as amortization), which can be as long as 30 years.

Do you need to get a current value of your property? Then you are going to need an appraisal. Banks and other lending institutions want to know the “current” market value of your home before they consider loaning money on the property. An appraiser checks the general condition of your home and compares your home…

Want to buy a home and don’t have a bucket load of money to pay cash – here’s 7 steps to home ownership. Step 1 – start saving your down payment…

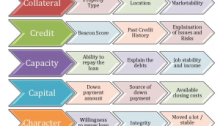

Five C’s of credit: Collateral, Credit, Capacity, Capital & Character help to determine a borrower’s ability and willingness to make payments. Understanding what a lender is looking for allows you to set yourself up to put your best foot forward.

Think of your credit score as a report card on how you’ve handled your finances in the past. A credit score is a number that lenders use to determine the risk of lending money to a given borrower. There is always someone willing to lend you money however, higher risk = higher rates!

For a first-time home buyer, the types of insurance surrounding a mortgage can be confusing, so it’s important to know what insurance covers what. There are 3 main types of insurance to know about when buying a home. Mortgage Default Insurance, Mortgage Insurance, and Life Insurance